Buy-to-Let property in the UK offers excellent yields with a good capital growth potential and it looks as though the trend is going to continue into the near future.

Browse our available BTL properties for sale or contact our team today on+44 (0) 161 337 3890to learn more about how Pure Investor can help you!

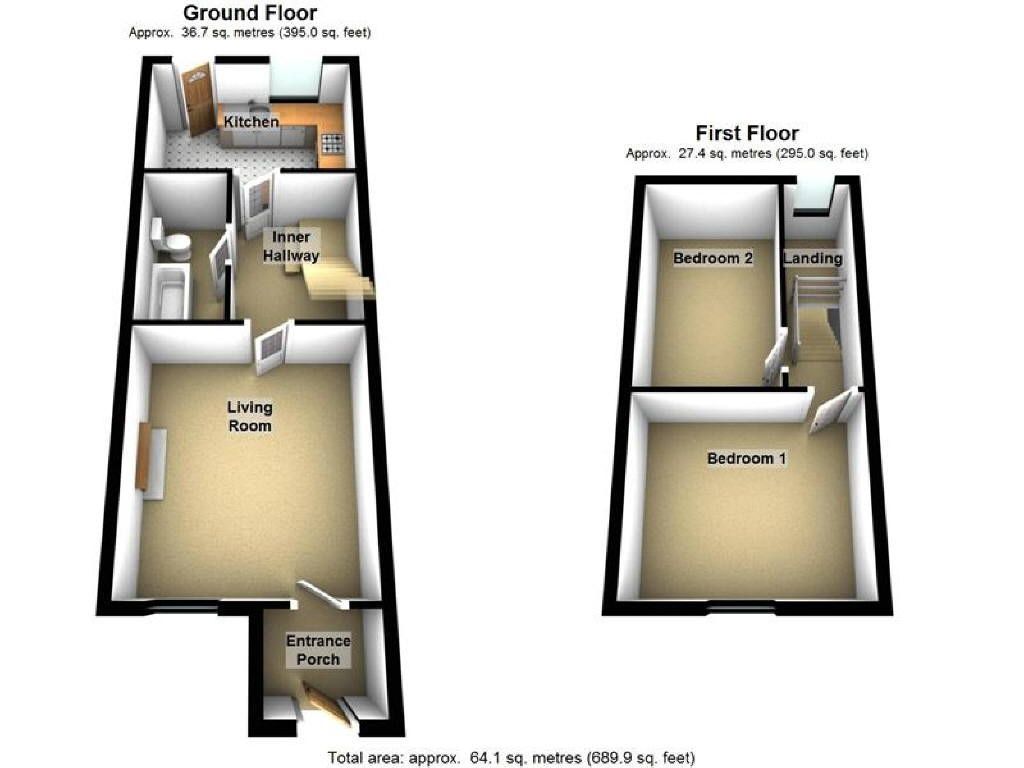

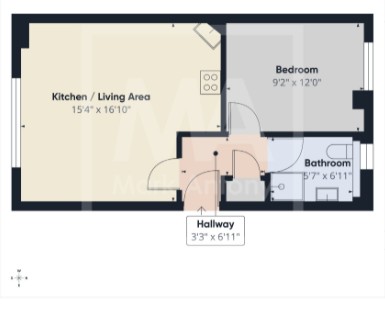

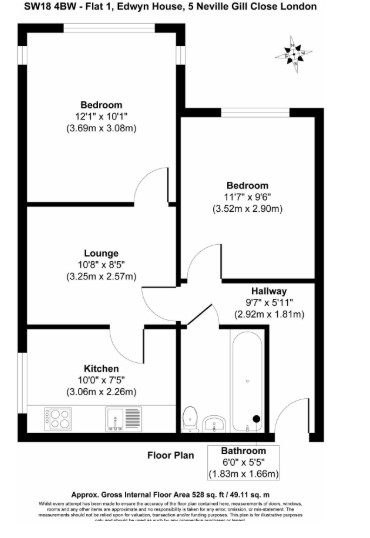

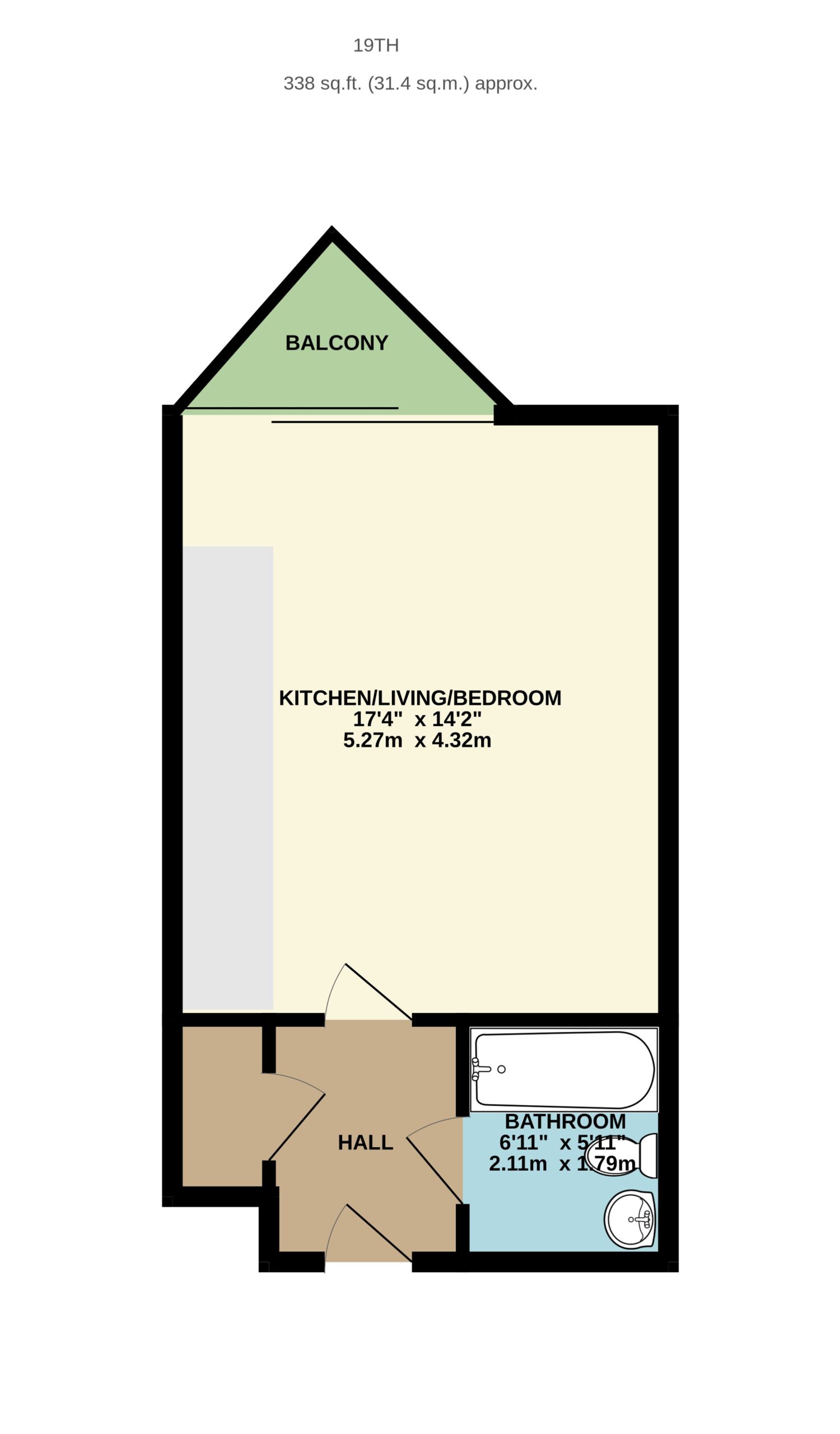

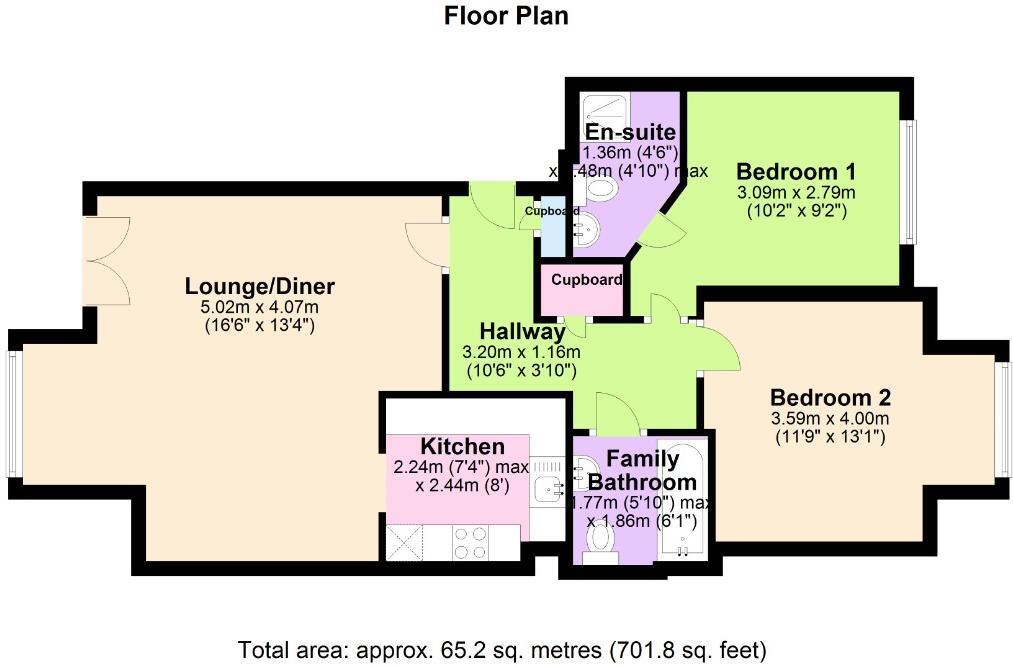

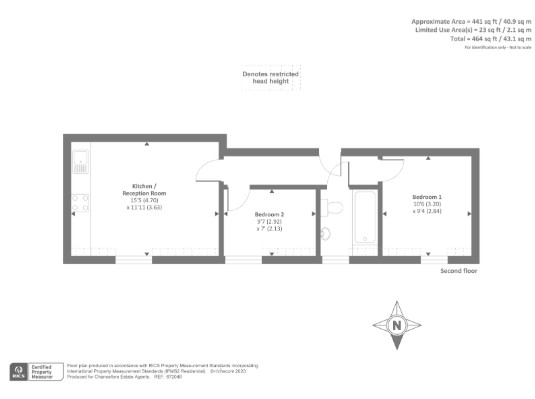

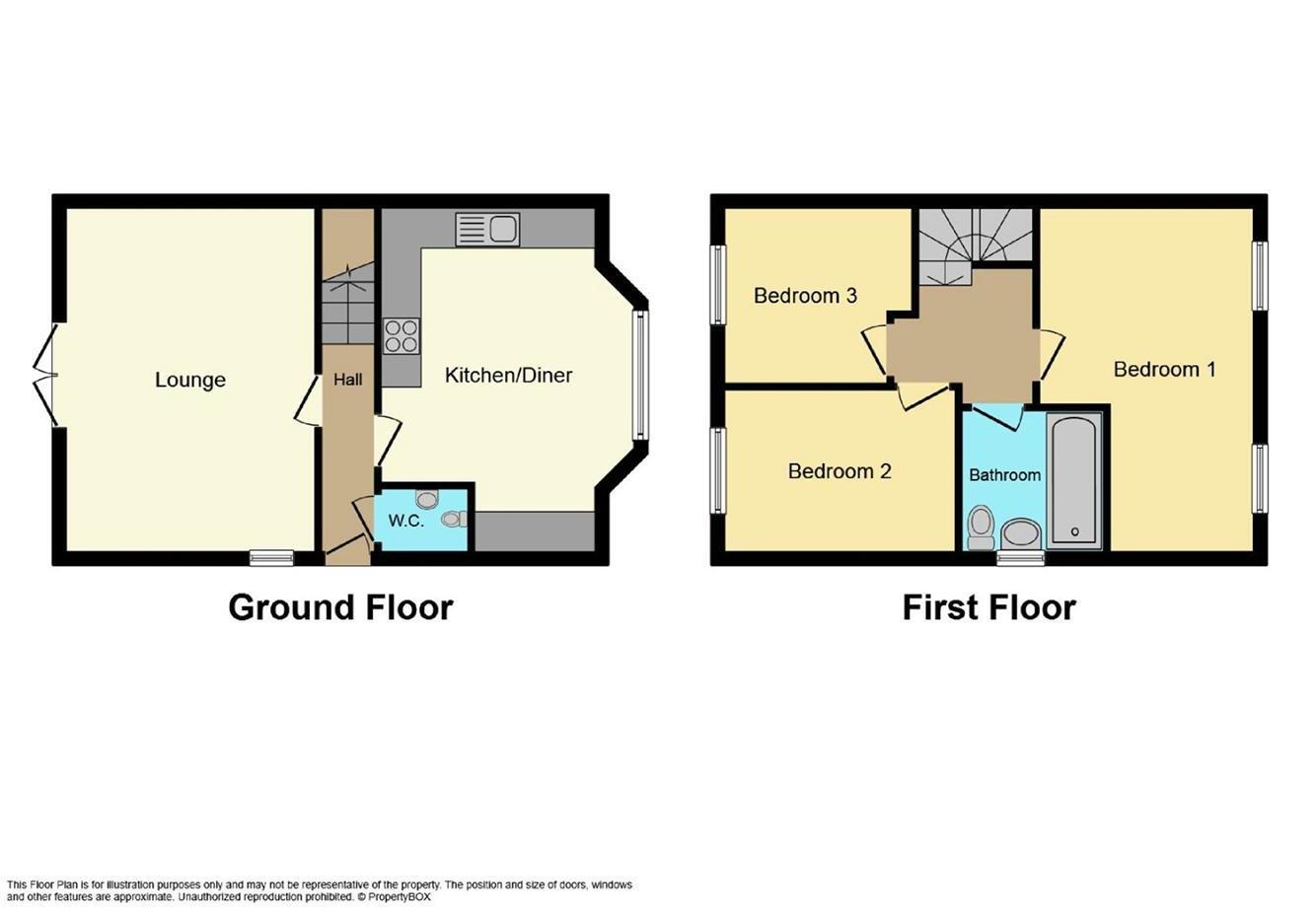

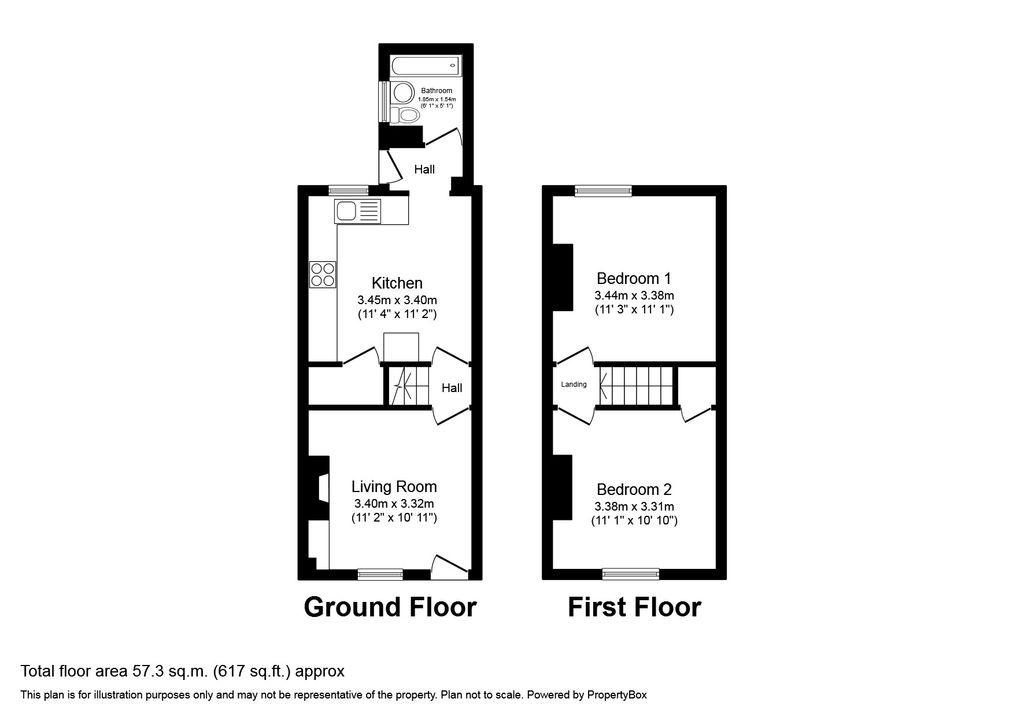

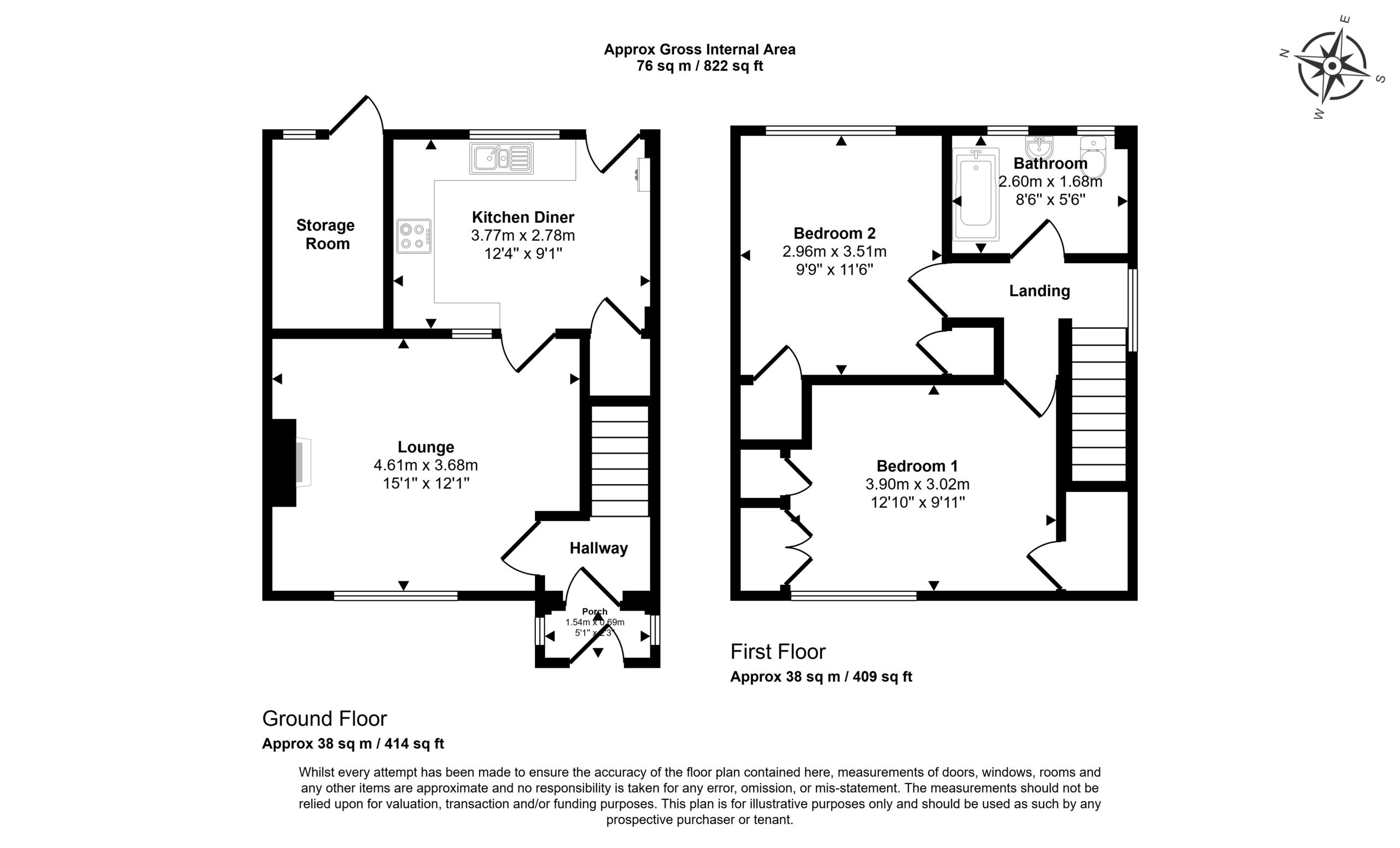

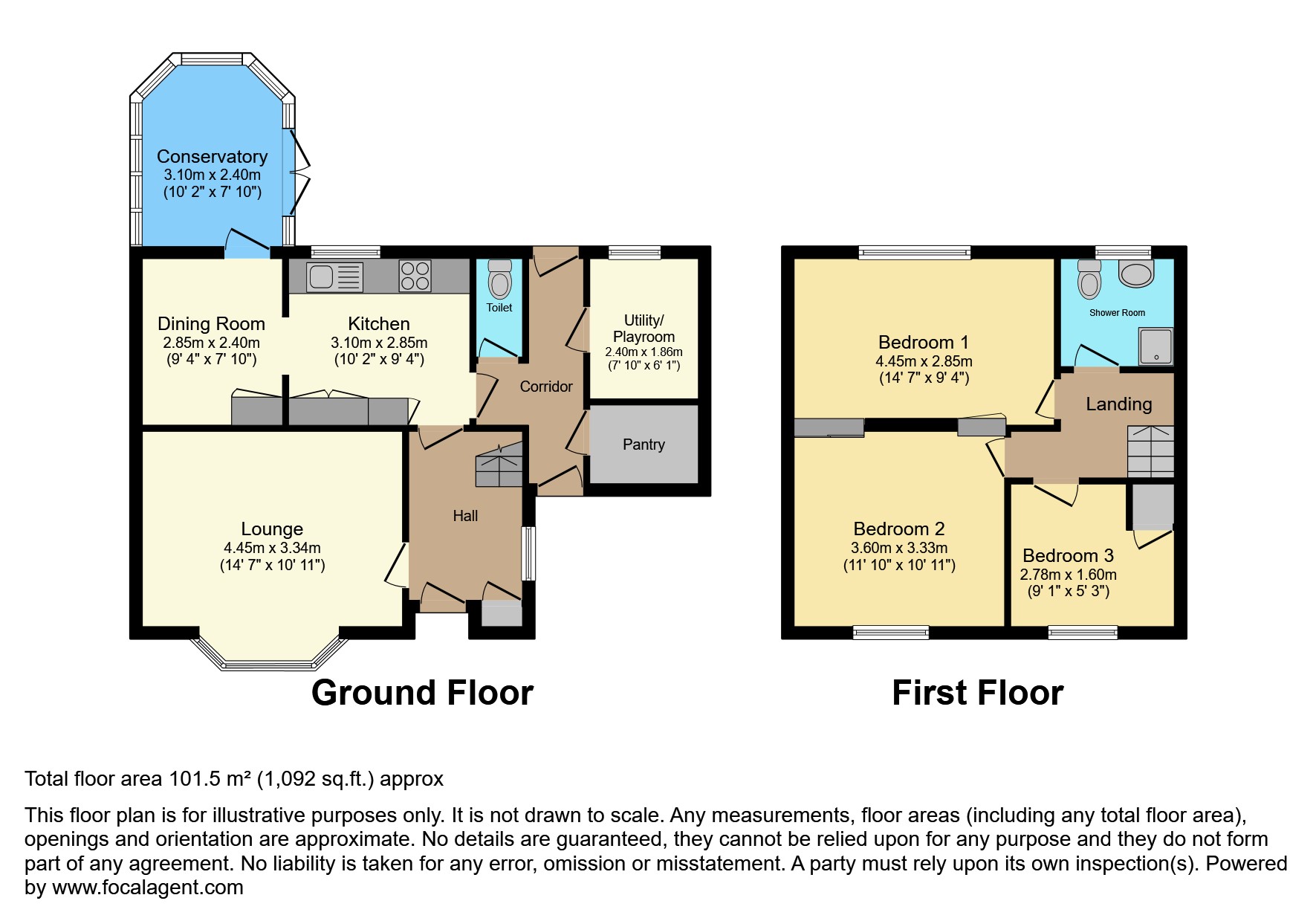

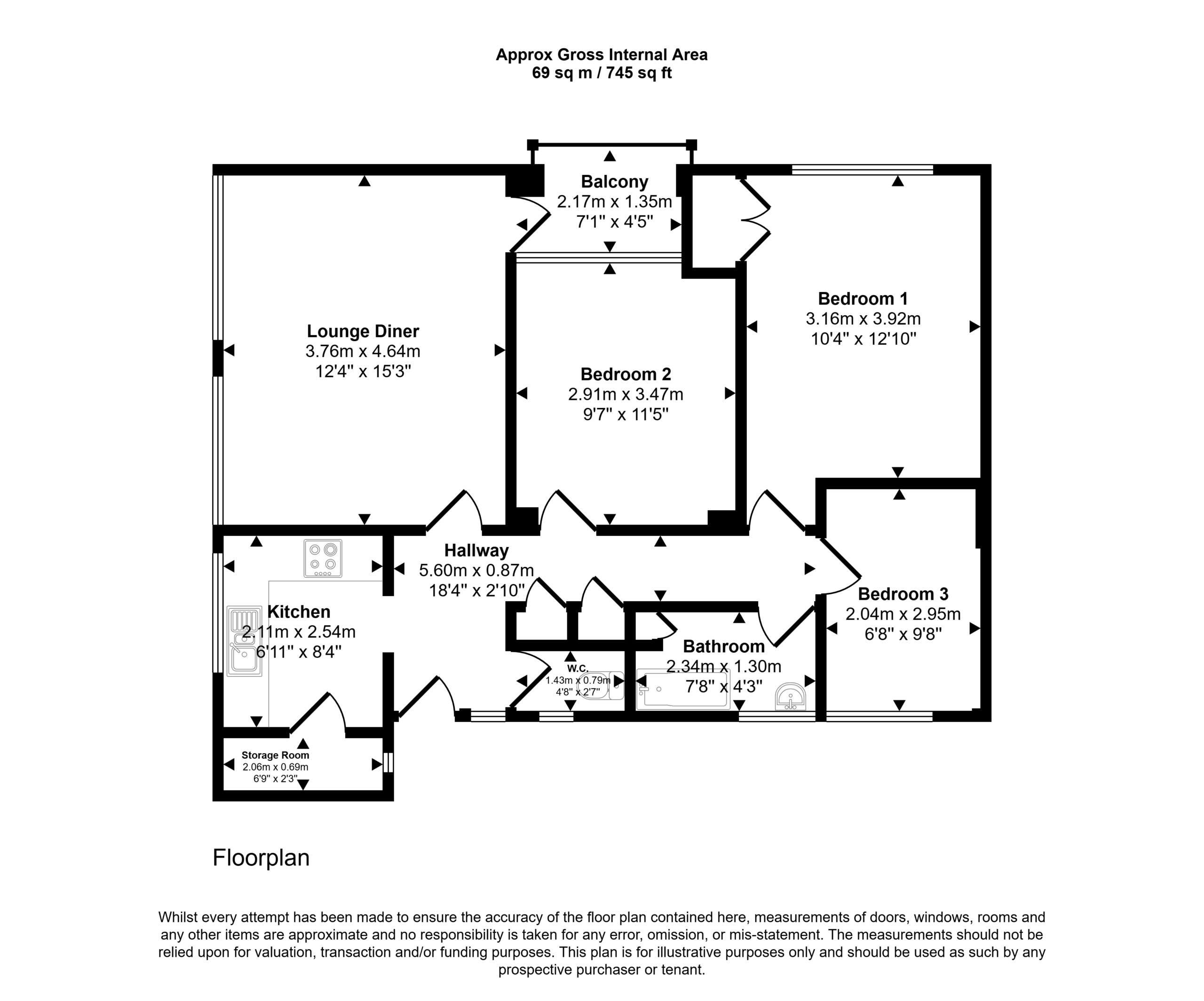

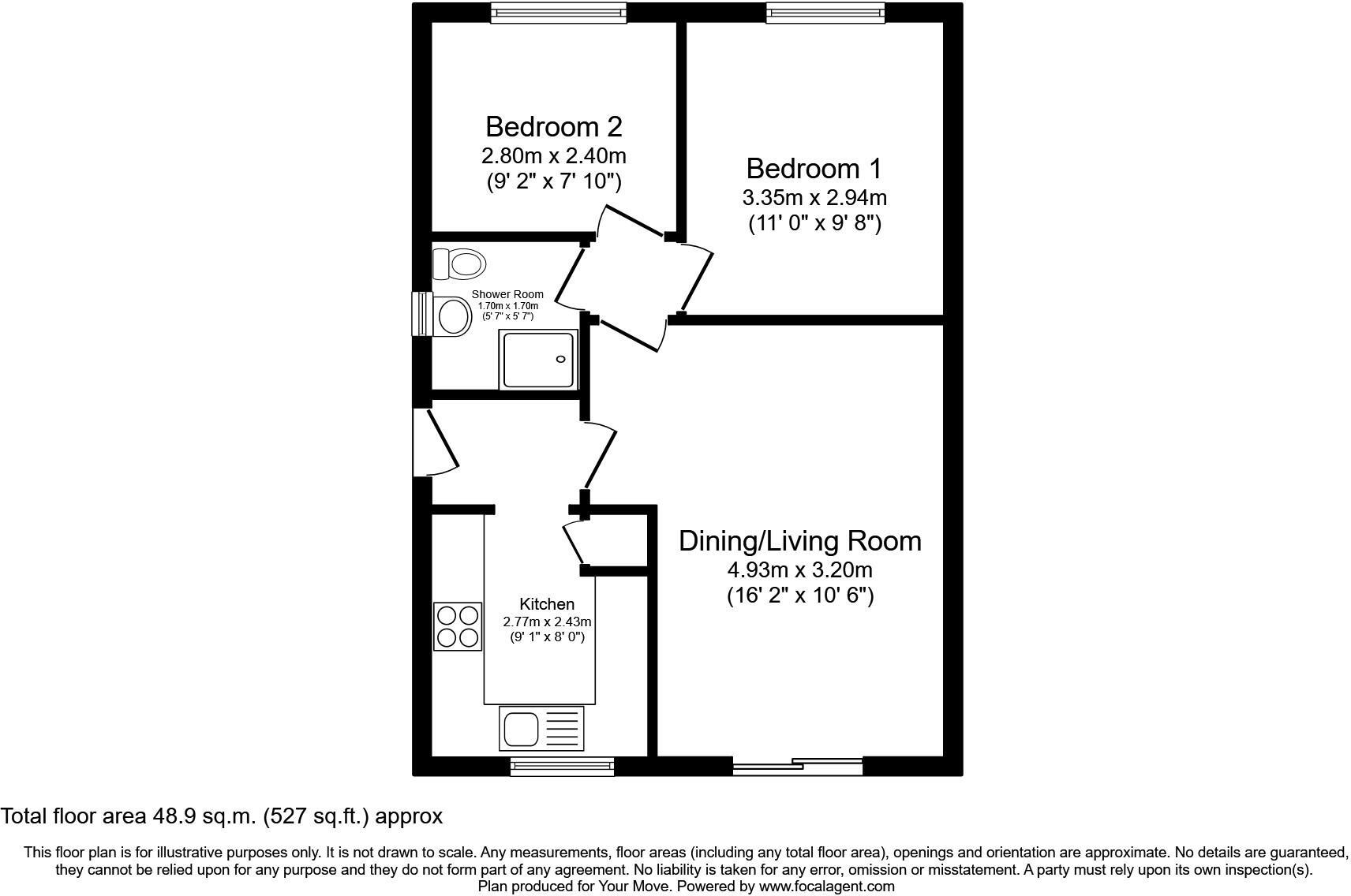

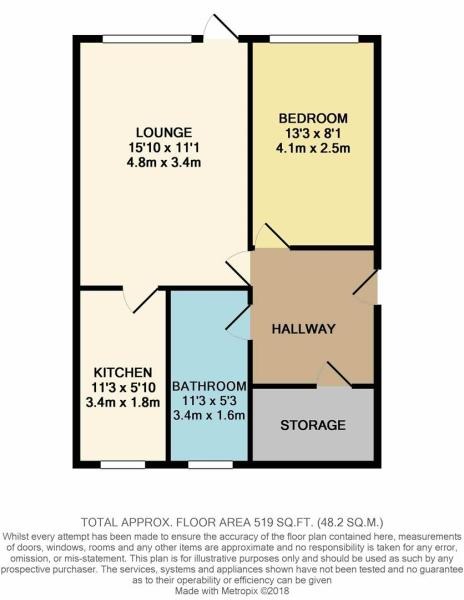

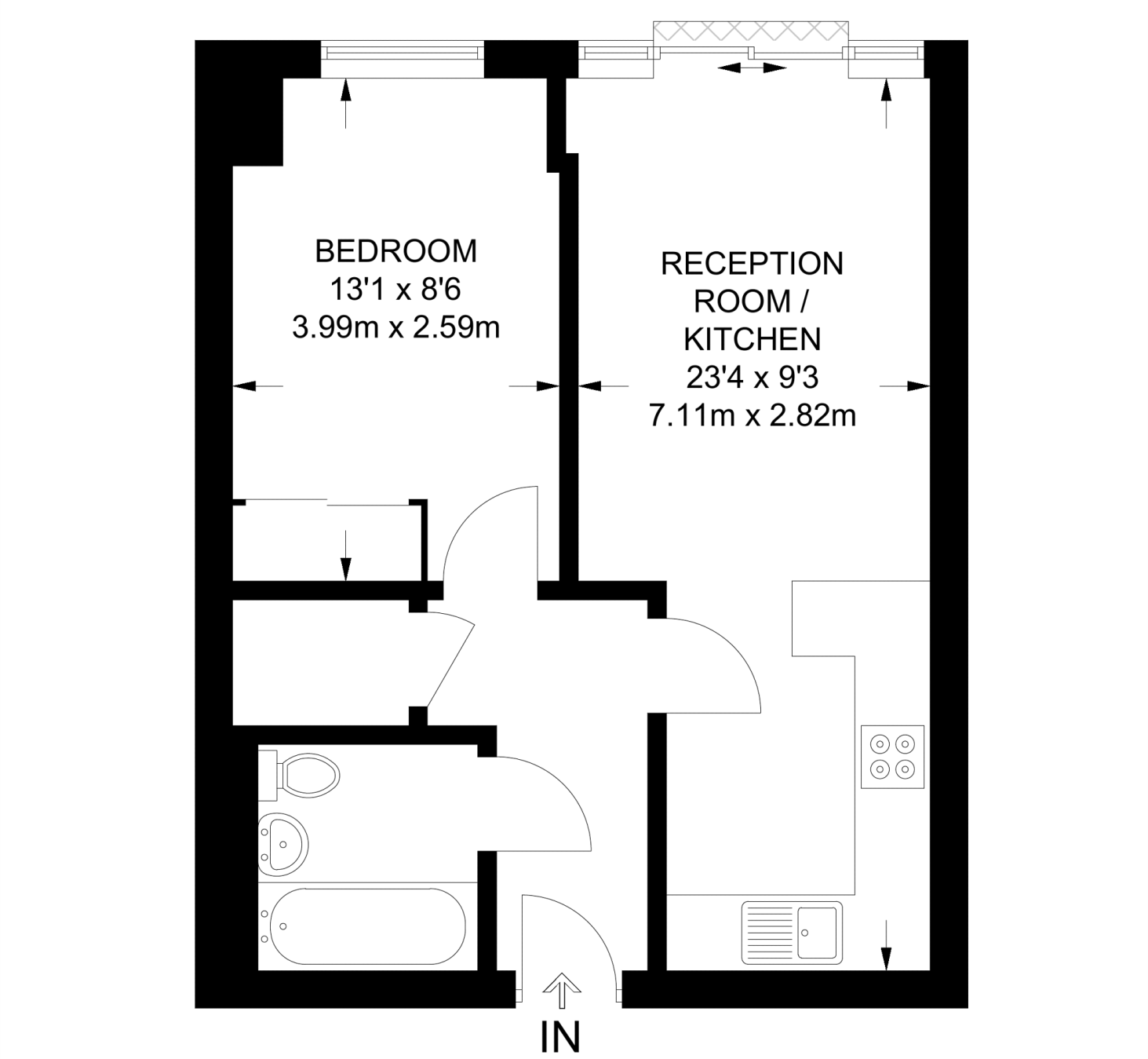

Buy-to-let property being sold with the current tenants in situ

Current tenant has been in situ since 2008

Current rental income of £550pcm generating 5.87% yield. Potential to bring this up to market rate of £700pcm which would generated an increase of 7.47% yield

Well maintained property, ideal first time investment or to expand property portfolio

Potential to earn immediate rental income from day one

Buy-to-let properties are becoming the chosen investment for many as they seek to find an asset where their money can work hard for them, providing high returns as well as offering a safe investment. The price of property in recent years has continued to increase in many areas of the UK and the same can be said for rental prices which make a buy-to-let investment even more appealing.

What is Buy-to-Let Property?

Buy-to-Let is a property investment strategy where investors purchase a property specifically to rent it out to tenants. This approach allows investors to earn rental income while benefiting from capital appreciation if the property’s value increases over time.

Investors can choose between short-term rentals, such as holiday lets, or long-term leases. To make the process more hands-off, many buy-to-let investors opt to hire property management companies to oversee the day-to-day operations, creating a passive income stream.

Why should you consider a Buy-to-Let Investment?

Buy-to-let investors have received returns of almost 10 per cent since 2000.

Buy-to-let property investments are popular among those looking to add to their pension.

The number of landlords has continued to increase, proving it’s an asset worth investing in.

Historically, purchasing property has been one of the safest ways to invest but it has also been one of the best performing investments and this still remains the same. A UK buy-to-let property investment brings together the benefits of a regular income along with capital appreciation in the long-term.

For those investors looking to make a buy-to-let property investment now is a great time to begin the process. Rental prices are increasing and yields of up to 10% can be achieved and in some cases more, especially if the right property is purchased.

When compared to the extremely low interest on savings it is easy to understand why investing buy-to-let properties is a popular choice with investors, but they are also driven by the potential capital growth in the medium to long-term.

If you’re interested in learning more about buy-to-let investments, continue below to read our comprehensive Buy-to-Let Property Investment Guide which will provide you with information on how to plan, research and begin your first (or next) buy-to-let investment.

For more information on our buy-to-let property investment service or if you need assistance in making the right investment decision, contact Pure Investor today.

Contact the Team

Call us on +44 (0) 161 337 3890 or contact us using the form below to arrange your free no obligation property consultation.

Our rental guarantee insurance offers our investors peace of mind by covering you for the loss of rental income. Our rental guarantee insurance is available for investors with tenants already in place.

Property in the UK is widely recognised to be a great investment, but actually getting started in property investment in the UK can be a bit of a daunting task even for locals, let alone for people who wish to invest from overseas.

In the absence of any clear idea of what is going to happen, astute investors will actively look for investment areas which have an above-average chance of thriving regardless of whether or not Brexit happens and, if it does, regardless of what form it eventually takes. Manchester is an obvious choice.

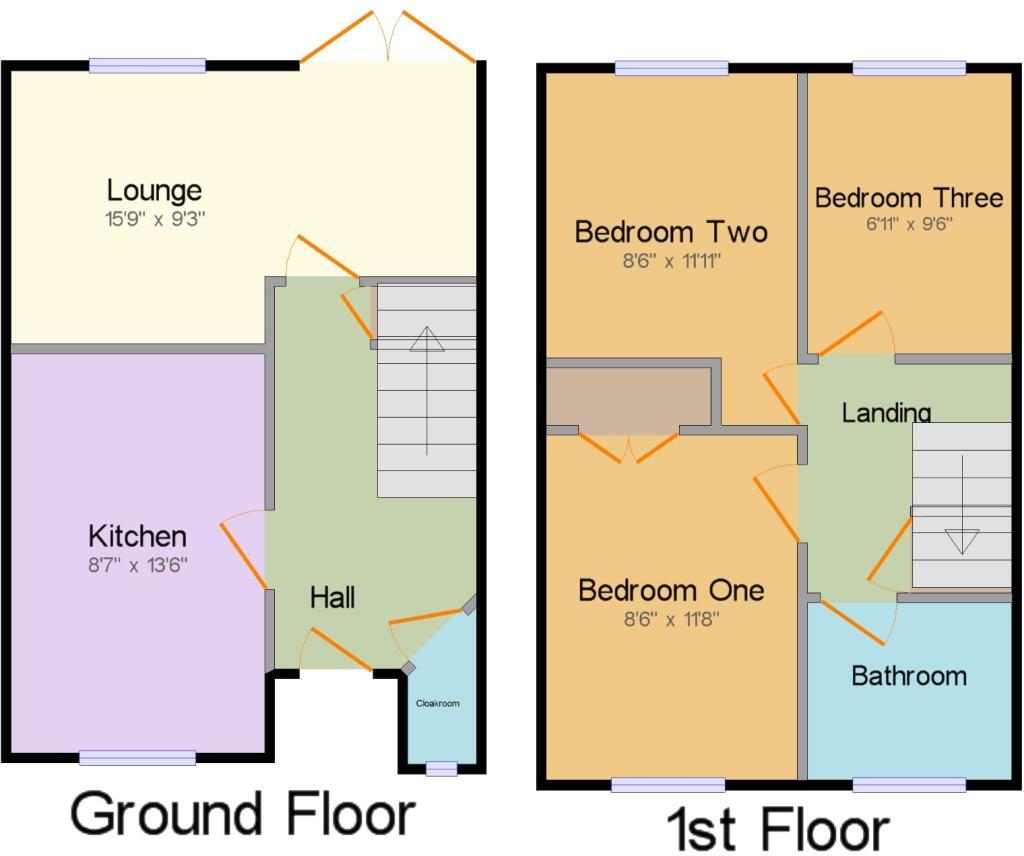

Thinking of selling your investment property? Learn the pros and cons of selling with tenants in situ vs. vacant possession, how to calculate yield, and tips for a fast sale.

Selling an investment property is fundamentally different from selling a main residence as buy-to-let. Landlords, property investors and owners of rental properties must navigate a distinct set of tax, legal and financial considerations.

This guide helps you put together a structured tenant selection process using UK-specific legal and practical advice to find good tenants for your properties.